When debt pressure becomes overwhelming, bankruptcy can do more than reduce balances with what bankruptcy stops—it can immediately stop many of the aggressive collection actions creditors use. For individuals and families across Pennsylvania, filing for Chapter 7 or Chapter 13 bankruptcy may trigger an automatic stay, a federal legal protection that can halt wage garnishments, foreclosure actions, repossessions, lawsuits, and creditor harassment.

At John M. Kenney, debtors receive urgent legal guidance designed to protect income, homes, vehicles, and peace of mind before irreversible financial damage occurs.

The moment a bankruptcy case is properly filed, an automatic stay under federal bankruptcy law usually goes into effect. This court-ordered protection requires most creditors to stop collection activity immediately.

In many Pennsylvania bankruptcy cases, this legal stay may stop:

This protection is often immediate, which is why timing is critical when deadlines are near.

Yes. In most cases, bankruptcy can stop wage garnishment as soon as the automatic stay takes effect.

If your paycheck is being reduced because of credit card debt, medical bills, judgments, or unsecured loans, filing bankruptcy may stop further garnishment quickly. For Pennsylvania workers facing mounting payroll deductions, this relief can restore necessary household income almost immediately.

How fast does wage garnishment stop?

In many cases, employers receive notice shortly after filing, and garnishments stop after the bankruptcy court notification is processed.

If wages are already being garnished, immediate filing may prevent additional deductions.

Yes. Bankruptcy may stop foreclosure proceedings, including scheduled sheriff sales, if filed before the foreclosure deadline.

A stop foreclosure bankruptcy attorney can often intervene before a Pennsylvania sheriff sale occurs.

Chapter 13 and foreclosure defense

Chapter 13 bankruptcy is especially powerful in foreclosure cases because it may allow homeowners to:

Chapter 7 and foreclosure

Chapter 7 may temporarily delay foreclosure, but it does not usually create a repayment plan to save delinquent mortgages long term.

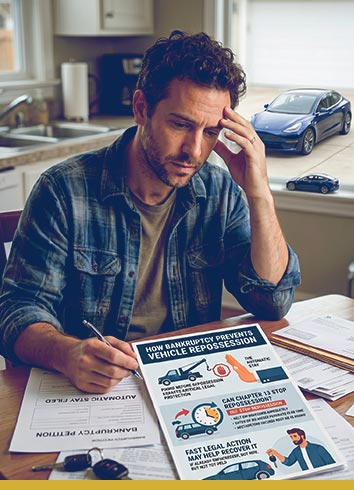

If repossession is threatened, bankruptcy may stop lenders from taking your vehicle once the case is filed.

For many debtors, filing before repossession occurs creates critical legal protection.

Can Chapter 13 stop repossession?

Yes. Stop repossession. Chapter 13 cases often allow borrowers to:

If the vehicle has already been repossessed but not yet sold, fast legal action may still help recover it in some situations.

Constant creditor calls create emotional exhaustion and legal stress. Bankruptcy often stops:

Once creditors receive notice of a bankruptcy filing, they must stop most direct collection communication.

Can creditors still call after bankruptcy is filed?

Generally, no. Continued collection calls after notice may violate bankruptcy law.

Yes, in many cases, bankruptcy may stop sheriff sales and bank levies if filed before enforcement occurs.

Sheriff sale deadlines matter

If your Pennsylvania sheriff sale is already scheduled, filing must occur before the sale is finalized.

Bank levies and frozen accounts

Bankruptcy may stop additional levy actions, although funds already seized before filing may not always be recoverable.

Immediate attorney intervention is often necessary when accounts are frozen.

Once the automatic stay begins:

However, the automatic stay is not always permanent.

Temporary stop vs permanent discharge

These are separate legal protections and should not be confused.

Waiting too long can eliminate legal options.

If any of the following are happening, immediate filing review is critical:

In emergency debt cases, hours can matter.

Stop creditor action before it’s too late.

In many cases, garnishment stops as soon as the bankruptcy filing triggers the automatic stay and notice reaches the employer.

Yes, if filed before the foreclosure sale is completed, bankruptcy may stop foreclosure the same day.

Not always. Chapter 7 may only delay repossession, while Chapter 13 may create long-term repayment protection.

Usually no. Once notified, creditors must stop collection calls under the bankruptcy law.

You may still be able to stop it if bankruptcy is filed before the sale occurs.

In qualifying cases, bankruptcy may temporarily prevent utility disconnection if filing occurs before shut-off.

Some IRS and state tax enforcement actions may pause temporarily, though exceptions apply.

It may stop future levy activity, but already seized funds may require separate legal review.

If creditors are threatening foreclosure, garnishment, repossession, or lawsuits in Pennsylvania, immediate bankruptcy filing may protect your assets and income today.

Call now for immediate bankruptcy protection.

Speak with a bankruptcy attorney today.

John M. Kenney helps Pennsylvania families act fast before financial threats become irreversible.